When a Legacy Claims System Fails, It Doesn’t Fail Slowly

Claims processing system modernization is not a technology problem. It is a comprehension problem. US carriers lose an estimated $35–70 million annually in claims leakage on a $500 million book [2].

The industry average cycle time sits at 40.7 days from FNOL to payment. Amica closes the same cycle in 11 days [3]. That gap is decades of adjudication logic sitting undocumented across hundreds of code modules, understood by a shrinking number of people, and moving silently toward a compliance event.

The loss environment makes the underlying system risk harder to absorb. Swiss Re placed 2025 global insured CAT losses at $107 billion, with 83% concentrated in the US market [1]. Six consecutive years above $100 billion.

Hurricane Milton alone generated 187,000 claims against $2.68 billion in replacement cost value, and cycle times stretched from 9.7 to 11.2 days, not because infrastructure buckled, but because legacy claims systems aren’t built to surface adjudication errors at scale.

When claim density spikes, every misfiring rule fires more often. Legacy systems built for normalized loss years are now running as permanent CAT infrastructure.

The core problem in claims processing system modernization is not which platform a carrier chooses or what timeline it budgets. It is that the adjudication logic accumulated over decades sits undocumented across hundreds of modules, and no program moves it safely without first understanding what it does.

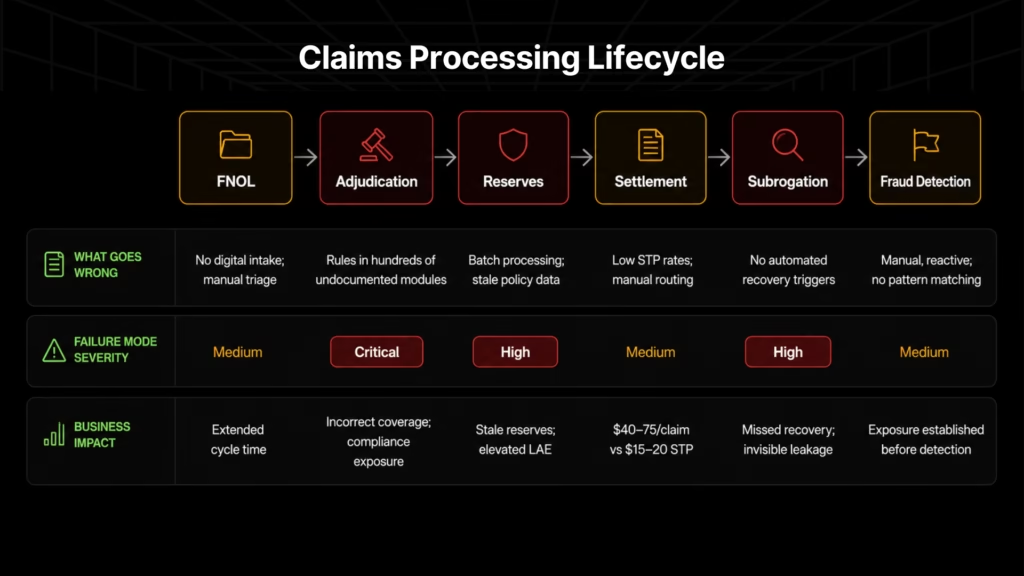

Where Legacy Claims Systems Break Down at Every Stage

A claims system is among the most tightly coupled systems in any enterprise. Policy administration, billing, underwriting, and fraud detection all intersect inside the claims workflow. The failure modes are stage-specific and they compound.

The table below maps the primary failure mode and measurable consequence at each stage.

| Claims Stage | Primary Legacy Failure Mode | Measurable Consequence |

| FNOL | No digital intake; manual triage; no structured data capture | Extended cycle time; depressed satisfaction scores |

| Adjudication | Rules distributed across hundreds of undocumented modules | Incorrect coverage decisions; compliance exposure; financial loss |

| Reserves | Batch processing; no real-time policy integration | Stale reserves; supplement rate inflation; elevated LAE |

| Settlement / STP | Low straight-through rates; manual processing | $40–75 per claim vs. $15–20 for STP |

| Subrogation | No automated recovery triggers; adjuster-memory dependent | Missed recovery — the most invisible leakage component |

| Fraud Detection | Manual, reactive review with no cross-claim pattern recognition | Irregularities go undetected until exposure is established |

FNOL

FNOL carries the lowest transformation risk of any claims stage. The logic is shallow in routing decisions, intake structure, or triage assignment. Nothing in FNOL digitization touches coverage determination or reserve calculation.

ValueMomentum’s 2026 benchmarking of 75 P&C carriers puts 40%+ citing leakage as a top operational challenge, with FNOL modernization frequently the first phase of an incremental program [4]. The mistake is treating FNOL completion as a proxy for adjudication readiness. It is not.

Adjudication

Adjudication is the stage this article must resolve. Failures at every other stage are operational, such as slower cycle times, elevated LAE, and missed recoveries. The failure mode at adjudication is existential: incorrect coverage determinations, incorrect payment calculations, and incorrect regulatory compliance. The next section develops this in full.

Reserves

Most legacy claims systems calculate reserves through batch processes that don’t pull current policy history at the time of loss. Integration gaps routinely add two to three days to reserve-setting.

One carrier that surfaced prior loss history directly in the adjuster screen cut supplement rates from 28% to 14% and reduced LAE per claim by roughly 9%. The mechanism was integration, not AI. And that result is unavailable when the claims system can’t reach current policy data in real time.

Settlement and STP

Manual processing costs $40–75 per claim. Straight-through processing brings that to $15–20. Moving from a 10% to a 30%+ STP rate generates ROI within two years for a mid-size carrier, but STP rates are gated by adjudication logic quality.

A rule that misfires doesn’t follow a straight-through process. It routes to manual review, inflating the per-claim cost the program was meant to reduce.

Subrogation

Legacy systems have no automated trigger logic to flag claims where recovery is likely. Recovery depends on adjuster memory and caseload. By the time an opportunity surfaces manually, the window has often narrowed or closed.

This is the literal definition of accumulated technical debt: eroded operational capability compounding silently, invisible on a balance sheet until it is quantified.

Fraud Detection

Manual, reactive fraud review has no mechanism for identifying patterns across claims over time. Irregularities go undetected until the financial exposure is already established.

AI-based detection identifies suspicious patterns weeks earlier than traditional methods, but those models require two or more years of clean historical claims data to mature, which makes the underlying data architecture a prerequisite, not an afterthought.

The Adjudication Logic Problem: Why This Is the Hardest Code in Any Claims System to Modernize

What the Accumulation Looks Like

A claims adjudication engine is not a system with a documented rule set. It is a three-decade accumulation of decisions made by regulators, compliance officers, litigators, product managers, and developers, each encoding a judgment call into the codebase, often without reference to what came before it.

Rules governing terminated products still apply. Conditions added after litigation outcomes in 2009 contradict conditions added after regulatory changes in 2014. None of it is written down anywhere outside the code.

The people who know why those rules exist are not the engineers who maintain the system today. They are claims attorneys who negotiated a settlement in 2007, compliance officers who responded to a state DOI inquiry in 2012, and actuaries who adjusted reserve triggers after a bad CAT year in 2017. Their decisions are in the codebase. Their reasoning is not.

The Workforce Retirement Accelerant

The engineers who carry undocumented exception logic in their heads are retiring. Why a coverage rule was hardcoded in 2003, or what litigation outcome changed a reserve calculation in 2011, is context that exists only in institutional memory. Any program that starts after those retirements are complete faces a baseline that was never captured.

McKinsey’s April 2026 analysis names this directly: undocumented product logic and semantic gaps that surface late in migration projects are the persistent modernization killers [5]. Agentic AI can reverse-engineer archaic decision logic within days versus months for a human SME, with 20–50% productivity gains on discovery and 15–90% on testing and reconciliation.

Why Platform Replacement Alone Doesn’t Solve This

When a carrier migrates to Guidewire ClaimCenter or Duck Creek, undocumented adjudication rules don’t migrate automatically. They get missed, rebuilt incorrectly, or continue firing from the legacy layer under the new platform.

McKinsey and BCG put the failure rate for large-scale core system transformations above 70%, with nearly 25% becoming full write-offs [5]. Those are comprehension failures, not technology failures.

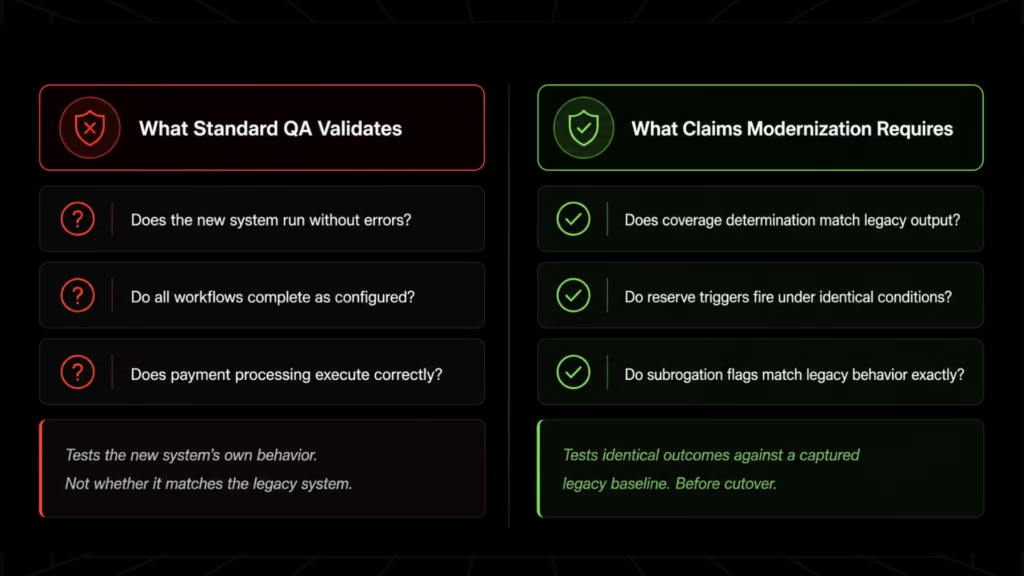

The QA Gap No One Names

Most QA validates what the new system does. It does not validate whether the new system matches what the old system did. A claims system that adjudicates slightly differently is not a QA finding, but a compliance event, a financial loss, and a potential policyholder dispute.

The adjuster running the new system has no way to know the rule has changed. The claims VP sees it three months later in the loss ratio. By then, the exposure is established.

Parity validation against a captured legacy baseline is the only testing model that closes this risk. Most programs skip that step.

The $0 Modernization Assessment produces the adjudication dependency map, risk heatmap, and modernization blueprint your program needs before any transformation decision. No cost. Delivered in days.

Three Modernization Paths for Claims Systems: What Each One Gets Wrong Without Comprehension First

The failure mode in the rightmost column is the same underlying problem expressed differently across all three paths.

| Path | Cost Range | Timeline | Primary Strength | The Real Risk |

| Platform Replacement (Guidewire, Duck Creek) | $5M–$50M+ | 18–36 months full platform; 6–18 months single module | Deep claims capability, cloud-native architecture, large partner ecosystem | Undocumented adjudication logic doesn’t migrate automatically — gaps surface as compliance events in production |

| AI-First Overlay | $500K–$5M per capability | 3–6 months per capability | Fast wins on targeted components; minimal disruption; measurable near-term ROI | Legacy adjudication still executes underneath; fraud models need 2+ years of data to mature; scaling risk deferred, not resolved |

| Comprehend and Modernize | Varies by codebase scope | Assessment: 3–5 days; transformation: phased | Only path where QA validates against a captured legacy baseline | Requires upfront comprehension discipline — programs under delivery pressure will try to skip it |

Path 1: Commercial Platform Replacement

Guidewire ClaimCenter and Duck Creek Claims are credible destinations. Cincinnati Insurance’s late 2025 ClaimCenter deployment on Guidewire Cloud for workers’ comp is a recent positive signal. The platform risk is not about product quality.

The risk is that custom adjudication logic doesn’t migrate through configuration alone. What implementation teams understand gets rebuilt; what they don’t get missed or deferred.

The platform runs correctly against its own configuration. Whether that matches the carrier’s actual adjudication intent is a separate question, rarely verified. Adjudication gaps surface later, as loss ratio anomalies, regulatory findings, or policyholder complaints.

Path 2: AI-First Overlay

Layering AI capabilities on top of a legacy claims core produces measurable improvements on the components it touches. Starting with intake before touching adjudication is a defensible sequencing decision for carriers that need near-term wins while a deeper program is being planned.

The constraint is what the overlay doesn’t reach. Fraud models need two or more years of claims data to mature. NLP intake processing doesn’t change downstream coverage determination. The legacy adjudication engine keeps executing underneath. Volume surges stress that core, not the overlay above it.

Path 3: Comprehend and Modernize

Before any carrier implements a platform, layers AI onto claims, or automates FNOL, it needs the adjudication rule catalog its legacy system has spent thirty years building and never written down. McKinsey and BCG both validate this sequencing as the correct approach for agentic AI in legacy modernization [5].

What that looks like in practice: A rules rationalization exercise at a P&C carrier, documented by insurtech firm SimpleSolve, became a full discovery exercise before any transformation could start [6].

Thousands of interdependent conditions were uncovered across modules that had not been reviewed since the early 2000s. Analytics dashboards had been misrepresenting operational reality because the actual decision logic sat below the reporting layer. Adjudicating claims one way while the reporting layer showed another.

The carrier had no accurate baseline. Without one, any platform they migrated to would have inherited the same errors in a more expensive system.

What Legacyleap does in a claims environment:

- The Assessment Agent surfaces what a carrier’s claims system actually does. It maps all dependencies across policy administration, billing, underwriting, and fraud detection, and identifies where transformation risk is concentrated. The output is a dependency map, risk heatmap, effort estimate, and migration blueprint, specific to the carrier’s codebase, delivered in three to five days through the $0 Assessment.

- The Documentation Agent reconstructs the adjudication rule catalog from the codebase itself: coverage determination logic, reserve calculation methods, subrogation triggers, fraud detection patterns, extracted and structured before any transformation begins. Not from documentation that may not exist. Not from SME interviews alone. From the code.

- The QA Agent generates a test baseline against the extracted legacy behavior: unit, integration, regression, API, and functional test cases at roughly twice manual authoring speed. Parity validation runs against that baseline, not the new system’s apparent behavior. Adjudication equivalence is verified before cutover, not inferred from go-live performance.

- The Modernization Agent executes governed code transformations as diff-based pull requests. No autonomous merges. No deployments without engineering review at each checkpoint. Roughly 70% automated; every transformation affecting product behavior requires human sign-off.

Legacyleap operates at the system level, codebase-grounded, agent-orchestrated, governed at every step. For a claims modernization ROI framework that accounts for adjudication risk, the comprehension investment is what prevents the far higher costs of production failure and program restart.

The Adjuster Adoption Problem

Claims adjusters have built years of operational knowledge around legacy systems, and not all of it appears in a requirements document. Custom exception-handling sequences, manual calculation workarounds, compensating behaviors for known system gaps: these are the real workflows a claims operation runs on.

Modernization programs that don’t account for them don’t fail at go-live. They fail three months after go-live, when supplement rates climb and productivity drops, and nobody can explain why.

The correct sequencing is

- Shadow testing with real adjusters before cutover,

- Workflow-by-workflow migration rather than full system replacement, and

- Hybrid interfaces during transition that let adjusters operate in both environments without losing velocity.

Adjuster input during the comprehension phase is what surfaces these failure modes before they become production events. The rule extraction process that the Documentation Agent runs is also the process that captures adjuster exception logic: the undocumented decision trees that adjusters have built around system gaps over twenty years of use.

If a modernization program has not involved an adjuster in the rule extraction process, it has not started yet.

Building the Claims Modernization Business Case

The financial model for claims modernization starts with a number most carriers already have internally and rarely formalize: their leakage rate.

EY’s March 2026 benchmarking places the range at 7–14% of total claims spend [2]. On a $500 million book, that is $35–70 million annually in overpayments, missed subrogation, and undetected fraud. A modernization program that reduces leakage by 30–50% (a conservative target for carriers moving from manual adjudication review to systematic rule extraction and STP automation) recovers $10–35 million per year.

| Claims Spend | Leakage at 7% | Leakage at 14% | 30% Reduction | 50% Reduction |

| $250M | $17.5M | $35M | $5–11M/yr | $9–18M/yr |

| $500M | $35M | $70M | $10–21M/yr | $18–35M/yr |

| $1B | $70M | $140M | $21–42M/yr | $35–70M/yr |

At a $5–15 million modernization investment for a single module replacement, break-even arrives within 12–24 months when leakage reduction is the primary metric.

The adjudication comprehension phase is what determines whether that recovery materializes, because incorrect rules migrated to a modern platform produce the same leakage at a higher operating cost. The platform investment is wasted without it.

The STP cost differential is the second lever. Manual claims processing runs $40–75 per claim. STP runs $15–20. At 100,000 claims annually, moving from 10% to 30% STP rate frees $5–11 million in processing cost.

Combined with leakage reduction, the business case for a mid-size carrier is typically net positive within two years, and front-loaded toward the carriers who do the comprehension work first.

The Adjudication Rule Catalog: The Document Every Claims Modernization Program Needs and Almost None Have

Claims modernization is a comprehension problem. The adjudication rules accumulated over decades in a legacy claims system determine every coverage determination, every payment, and every recovery. No path executes safely without those rules being extracted and documented first. For carriers considering full-stack insurance modernization, the adjudication rule catalog is where that work begins.

Programs that skip this step don’t fail at go-live. They succeed at go-live, then surface incorrect adjudication outcomes months later. The failure is deferred, not avoided.

The $0 Modernization Assessment produces the adjudication dependency map, risk heatmap, and modernization blueprint before any transformation decision. No cost. Delivered in days.

To see how Legacyleap’s agents work inside a claims environment, Book a Demo.

FAQs

Claims processing is the end-to-end lifecycle, from intake, investigation, reserve-setting, payment, to recovery. Claims adjudication is the specific determination of whether a claim is covered, to what extent, and at what amount. It is the most rule-intensive stage of the lifecycle and the one where legacy systems carry the highest concentration of undocumented logic. A modernization program can improve every other stage without touching adjudication, but the financial and compliance risk sits in adjudication, not in intake or payment.

They do not migrate automatically. Custom rules built over decades through regulatory responses, litigation settlements, and product changes must be manually identified, mapped, and reconfigured in the new platform. Rules that are not identified are either rebuilt incorrectly, missed entirely, or continue executing from the legacy layer in parallel. The most common failure mode is that a platform migration completes successfully on its own terms while a subset of adjudication logic quietly misfires, surfacing as loss ratio anomalies or compliance findings months after go-live.

Leakage quantification typically requires cross-referencing claims outcomes against what adjudication rules should have produced, which is difficult when those rules are undocumented. The practical starting point is running an adjudication audit against a sample of closed claims: comparing actual payments to policy terms, identifying supplement patterns, and reviewing subrogation outcomes against flagging criteria. EY’s March 2026 benchmarking puts leakage at 7–14% of claims spend for large carriers, which provides an external reference range for internal modeling. The $0 Modernization Assessment produces a dependency map and risk heatmap that identifies where leakage risk is concentrated before any transformation investment is made.

Loss adjustment expense (LAE) is the cost of investigating and settling claims: adjuster time, legal fees, expert fees, and administrative overhead. Legacy systems inflate LAE in two ways: they require more manual intervention per claim (raising adjuster cost), and they produce stale reserve estimates that lead to supplement payments when the initial reserve is wrong. One carrier that integrated real-time policy history into the adjuster screen reduced supplement rates from 28% to 14% and cut LAE per claim by roughly 9%. Reducing LAE does not require a full platform replacement. It requires eliminating the integration gaps that force adjusters to operate without current data.

The prerequisite is extraction before transformation, systematically analyzing the codebase to reconstruct what the adjudication engine actually does before any migration begins. This means cataloging every coverage determination rule, reserve trigger, and subrogation condition, including logic for terminated products and rules added in response to specific litigation outcomes or state DOI requirements. Human SME review of the extracted catalog against institutional memory is the validation step, but it requires that a structured catalog exists first. Transformation without that catalog does not preserve decades of embedded decisions. It discards them unknowingly.

References

[1] Swiss Re, sigma: Natural catastrophes in 2025, December 2025.https://www.swissre.com/institute/research/sigma-research/sigma-2025-natural-catastrophes.html

[2] EY, Insurance claims leakage: Stopping the drain on profitability, March 2026.https://www.ey.com/en_us/insights/insurance/claims-leakage-profitability

[3] JD Power, 2026 U.S. Property Claims Satisfaction Study, 2026.https://www.jdpower.com/business/press-releases/2026-us-property-claims-satisfaction-study

[4] ValueMomentum, 2026 P&C Insurance Claims Benchmarking Report, 2026. https://www.valuemomentum.com/resources/2026-pc-claims-benchmarking-report

[5] McKinsey & Company, Can agentic AI finally modernize core technologies in insurance?, April 2026.https://www.mckinsey.com/industries/financial-services/our-insights/can-agentic-ai-finally-modernize-core-technologies-in-insurance

[6] SimpleSolve, Insurance Palimpsest: Why Layered Processes Hide the Real System, March 2026.https://www.simplesolve.com/blog/why-layered-insurance-processes-hide-the-real-system